PakAlumni Worldwide: The Global Social Network

The Global Social Network

Post Cold War Geopolitics Keeps Indian Economy Afloat

India runs massive current account deficits. Its imports far outstrip exports year after year. According to the Reserve Bank (RBI) data, in the April-December 2014 period of last fiscal, India's current account deficit stood at $31.1 billion or 2.3% of GDP.

In spite such large recurring deficits, India has built up over $300 billion in foreign exchange reserves. How does it do it? The simple answer is: Foreign money inflows in the form of debt and investments mainly from the West keep the Indian economy afloat.

|

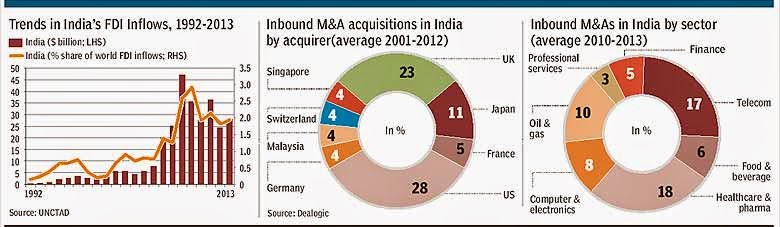

| Sources of FDI in India Source: Financial Express |

These inflows have dramatically increased with western support for India in the post Cold War world. Here's how Indian journalist Pankaj Mishra explains the larger western interest driving this phenomenon:

"Seen through the narrow lens of the West’s security and economic interests, the great internal contradictions and tumult within these two large nation-states (India and Pakistan) disappear. In the Western view, the credit-fueled consumerism among the Indian middle class appears a much bigger phenomenon than the extraordinary Maoist uprising in Central India".

Here's how the Asian Development Bank (ADB) describes the rising inflows of foreign, mainly western, capital into India:

"Gross capital flows have increased nearly 22 times from $42.7 billion in 1991-92 to over $932.3 billion in 2010-11. As a share of GDP, this amounted to an increase from 15.5% in 1991-92 to 55.2% in 2010-11. Much of the increase in financial integration occurred between 2003-04 and 2007-08. Given the impressive economic performance indicated by close to 9% growth rate, higher domestic interest rates and a strong currency, India's risk perception was quite low during 2003 to 2007. Furthermore, this period was associated with favorable global conditions in the form of ample liquidity and low interest rates in the global markets—the so-called period of Great Moderation."

Many other economies have been growing faster and producing higher investor returns than India. So the returns do not justify the increased capital flows. Such flows are driven much more by the changing geopolitics of South Asia region and the world since the end of the Cold War in early 1990s. Without these inflows, Indian economy would collapse and India would be at IMF's door seeking last resort loans.

Lesson: Geopolitics drive economy. It's the reason for over a trillion dollars of western capital flow into India since the end of the Cold War. It also explains China's massive $46 billion investment commitment in Pakistan agreed during President Xi Jinping's state visit to Islamabad.

Related Links:

How Strategic Are China-Pakistan Ties?

India Pakistan Economic Comparison in 2014

Pakistan's KSE-100 Outperforms India's Sensex

Views: 700

-

Comment by Riaz Haq on April 21, 2015 at 4:37pm

-

While the global financial crisis initially contributed to a slowdown in FDI inflows, the rather sharp downward trend and the consequent sluggish recovery of FDI that can be observed in the post global financial crisis phase has primarily been a result of a host of domestic factors.

Policy challenges on multiple fronts, including issues of governance, inadequate structural reforms, tax and political uncertainties, all contributed to the lacklustre performance of FDI in India.

While there are signs of stabilisation in net FDI inflows, India still has a long way to go to return to the pre- global financial crisis peak. In this light, it is not surprising that the Modi government has reiterated that the country’s FDI regime is highly open and conducive for attracting such flows of foreign capital.

Until 2012, about 40% of FDI inflows used to come from Mauritius, just under 10% from Singapore, and another 5% from the Netherlands.

These tax havens and offshore financial centres (OFCs) together made up just over half of all FDI inflows to India. In 2013, however, the composition changed, with Singapore’s share rising to 25% (boosted by the double taxation avoidance agreement the two countries have signed which has incorporated a Limitation of Benefit—LoB—provision), Mauritius with about 20% and the Netherlands at around 5%.

While Singapore and Mauritius have swapped places as top investors in India, still about 50% originates from these offshore financial centres. Clearly, these are not the original sources of external financing with the offshore financial centres responsible for a degree of round-tripping of funds from India and transshipping of funds from third countries. Accordingly, an analysis based on such data can be quite misleading when trying to understand economic linkages between countries.

If one wants to get a sense of the original source of these FDI flows, i.e. who is actually doing the investment in India and to understand the de facto real linkages at the bilateral level, mergers and acquisitions (M&A) data could offer a better, albeit partial, picture for that purpose. This is so as M&A data are based on actual ownership of the company as opposed to flow of funds. The M&A data only include direct investment that is foreign in nature and not merely round-tripping back to India from domestic sources.

However, one has to be careful in comparing M&A versus FDI data. First, not all FDI are M&As as they could be greenfield investments as well. Second, M&A transactions do not necessarily result in international capital flows across borders (for example, swapping of shares). Third, M&A data refer to the total deal value as at the date of completion though the deal value may be paid out over a number of years. Fourth, unlike FDI data, M&A data do not include retained earnings (which is a significant share of global FDI flows).

A comparison of the available FDI data to M&A data for India reveals an entirely different picture (figure 2). Countries like the US and the UK together make up 50% of M&A acquisitions into India, and Japan is responsible for another 10%. This triad is effectively responsible for three-fifths of FDI inflows into India (of the M&A variety at least). This provides us a more useful geographic breakdown of who is actually doing the investments in India.

A sectoral analysis of FDI inflows suggests that, on average, between 2000 and 2012, more than 35% of FDI inflows have gone into services, telecom and construction sector, with pharmaceuticals, chemicals and computer sector each receiving about 5% of the country’s total FDI inflows over the corresponding period. However, M&A data at the sectoral level for the same time span suggests telecom and pharmaceuticals (and healthcare) have attracted over one-third of the foreign M&A acquisitions in India. Of late, pharmaceuticals has attracted a greater share of M&As, with the sector taking about 20% of inbound M&A acquisitions between 2010 and 2013 (figure 3).

What does the foregoing discussion imply for policy? Obviously, first and foremost there is a need for better appreciation of the actual sources and destinations of FDI to and from India as well as the sectoral composition of FDI flows. In fact, while not discussed here, as Indian companies invest overseas more aggressively, better quality data on gross inflows and outflows at country and sectoral levels are needed.

Much more attention is also needed with regard to FDI quality at a more disaggregated level (i.e. new FDI versus retained earnings and greenfield versus M&A). While it is important for India to attract FDI, it is pertinent to ask the question whether a policy to attract FDI should be careful in distinguishing between the kind of FDI it wants to attract. All FDI are not the same and are not attracted by the same factors. The prime objective must be to align FDI with national development objectives, consistent with being an open economy.

http://www.financialexpress.com/article/fe-columnist/fdi-inflows-wh...

-

-

#India Worst performing stock market? This is the end of the Modi bubble for FIIs

Is PM Narendra Modi running out of luck? He had famously boasted being a lucky Prime Minister while seeking votes during the Delhi elections. The context, of course, was international oil prices had less than halved and that seemed to have brought all round uptick in economic sentiment, what with the stock markets soaring to new highs early 2015. Consensus among global FIIs was that they will remain overweight India as compared to other markets like China, Brazil, South Korea, Taiwan and Russia. But everything seems to be reversing over the past month and a half.

Suddenly the FIIs, with a cumulative investment in Indian stocks of about $300 billion at market value, are looking at other emerging stock markets for returns and no longer treat India as the most preferred destination as they did last year, and even the beginning of this year. FII net outflows gave been of the order of Rs 12,500 crore over the past month. The stock market index has seen the biggest correction of 10 percent in a short time. This has caused speculation whether the markets are slipping into a bear phase.

But what is indeed worrisome is India is probably the worst performing stock market among emerging economies this year. This is in sharp contrast to the view taken by the big FIIs that the Modi government reforms could trigger a multi-year bull run in India. Now the same FIIs are shifting the weightage of their global allocation to China where the stock markets have shown 30 percent growth since January. India's Sensex growth remains in negative territory. Even FII inflows, which primarily influence market movement, are flat to negative since January.

Worse, now FIIs also seem to prefer oil exporting markets like Russia and Brazil, both of whom had fallen out of favour after the global oil prices had more than halved, badly affecting their revenues. Now the FIIs believe that oil prices are moderately correcting and returning to oil exporting markets like Russia and Brazil makes sense. This view is buttressed by another major consideration. They feel as the US economy recovers and the prospect of monetary tightening by the Federal Reserve brightens, the dollar would strengthen in the short to medium term.

The Economic Times has just reported a survey of top CEOs and the majority of them suggest that demand is depressed. "The bonhomie and cheer that greeted the arrival of the Modi government is replaced by a sombre mood and a grim acknowledgement of the realities of doing business in India," reports ET, as it captures the sentiment of the CEOs. Little wonder that this is reflecting in the behaviour of the stock market and currency. The largest engineering conglomerate L&T had said some of its plants are lying idle as demand for capital goods is very weak. The Aditya Birla Group had deferred its revenue target of $65 billion by 3 years, to 2018.

These are not good signs for the economy and both the stock market and currency will reflect this in the months ahead.

http://www.firstpost.com/business/worst-performing-stock-market-end...

-

-

#India's August exports shrink for ninth straight month, fall 20.7%. #Modi #BJP http://toi.in/SejmIb

NEW DELHI: Contracting for the ninth month in a row, India's exports plunged by 20.66 per cent in August to US $21.26 billion, widening the trade deficit.

READ ALSO: Devaluation of yuan will affect India's textile exports

The significant slump in country's exports is attributed to global slowdown and declining commodity prices worldwide.

In August 2014, the merchandise exports had amounted to US $26.8 billion. The last time exports registered a positive growth was in November 2014, when shipments had expanded at a rate of 7.27 per cent.

Imports too declined by 9.95 per cent to US $33.74 billion in August this year due to high gold imports, leaving the trade deficit at US $12.47 billion, according to the data released by the Commerce Ministry.

However, the trade deficit has narrowed in August as compared with July this year, when the figure stood at US $12.81 billion.

In August last year, the deficit was US $10.66 billion.

Gold imports rose by 140 per cent to US $4.95 billion in the month under review from US $2.06 billion in August last year.

The main exporting sectors which reported decline in exports include petroleum products (fall of 47.88 per cent), engineering (29 per cent), leather and leather goods (12.78 per cent), marine products (20.83 per cent) and carpet (22 per cent).

Exporters expressed concerns over the continuous decline.

-

-

#Credit Rating: #India Doesn't Deserve To Be Equal To #China #China rated close to #US, #India near junk via @forbes

http://www.forbes.com/sites/panosmourdoukoutas/2017/02/05/india-doe...

India doesn’t deserve to be next to China — when it comes to credit rating agencies that is.

That’s according to all major credit agencies, which give China a near perfect score — close to the US — and India a near junk score. Fitch, for instance, gives China A+, and India BBB- (see table).

China’s and India’s Credit Rating

India’s credit rating lag behind China is also reflected in credit markets, where the Indian government has to pay almost twice as much as China to borrow money for ten years—see table.

That’s certainly upsetting to India’s government officials, who blame credit agencies for favoring China over India. Specifically, they are critical of the agencies for failing to lift India’s credit rating despite its improving economic fundamentals, like robust economic growth rates and fiscal discipline.

At the same time, they point to the fact that the agencies have failed to lower China’s rating in spite of deteriorating fundamentals like – the slowing down of the economy and soaring debt to GDP ratio.

------

China has a recent history of current account surpluses and enormous foreign currency reserves, while India has a recent history of current account deficits and moderate foreign currency reserves. This means that China lives below its means, while India lives beyond its means.

That’s a situation that may become worse with Narendra Modi’s free cash for everyone, which is expected to turn India into next the Brazil.

Persistent current account deficits make India more vulnerable than China to the next global crisis – one that, should it occur, will shift the tides of foreign capital flows from emerging countries back to developed countries—a big concern for the credit rating agencies and foreign investors that rely on them.

The bottom line: To move next to China in the credit rate scale, India must learn to live within its own means.

-

-

#IMF says #India vulnerable for depending on foreign money to finance public #debt, #trade #deficit http://ecoti.in/w-xtyZ @economictimes

India needs to remain vigilant as greater reliance on debt financing and portfolio inflows could create significant external financing vulnerabilities, a recent IMF report has said.

The The International Monetary Fund (IMF) in its report titled 'The 2017 External Sector Report' further said other risks to the Indian economy stem from global financial volatility and 'longer-than-expected cash normalization' following the currency exchange initiative.

"Like other EMs, too too great a reliance on debt financing and portfolio inflows would create significant external financing vulnerabilities. Therefore, there is need to remain vigilant to safeguard the Indian economy.

"...India's economic risks stem from intensified global financial volatility including from a faster-than-anticipated normalization of monetary policy in key advanced economies, longer-than-expected cash normalization following the currency exchange initiative, as well as slower global global growth," the report noted.

India's Monetary policy framework has been strengthened, the report said, adding, "but further supply-side reforms and continued fiscal consolidation are key requirements to achieve a low and stable rate of inflation in the medium-term as well as to keep gold imports contained."

Emphasising that continued fiscal consolidation is needed, which includes implementation of the goods and services tax and further subsidy reforms, the report s ..

Read more at:

http://economictimes.indiatimes.com/articleshow/59848585.cms?utm_so...

-

-

The great Indian trade-off

Sluggish exports leave India needing to curry favour with investors

Perennial domestic weakness, and America’s recent protectionist turn, make it hard for India to sell more abroad

https://www.economist.com/news/finance-and-economics/21742008-peren...

In the 12 months to March 2018, $303bn of Indian goods ended up overseas. That was up on the previous year, but still short of the $310bn achieved in 2014, when the Indian economy was a quarter smaller. Imports, meanwhile, have increased to $460bn, pushing the merchandise deficit to $157bn last year, up from $109bn in 2016-17 and its highest level in five years. A surplus in services such as IT outsourcing helps reduce the overall trade deficit by around half, but even there imports are growing faster than exports.

The shortfall is swollen by the rising price of oil, lots of which India imports (and some of which is also sold on as refined products). The surge from around $30 per barrel in early 2016 to over $70 now goes a long way to explaining the rise in India’s current-account deficit, which is expected to reach 2% of GDP this fiscal year, triple last year’s reading. Gold imports, used for saving or jewellery, have their own unpredictable rhythms, but also deepen the deficit.

The current trade lull extends beyond gold and oil, however. Exporters across the economy are being squeezed by the poor implementation of a goods-and-services tax that came into force last July. Perhaps 100bn rupees ($1.5bn) of refunds due to exporters once they can prove they have shipped their wares abroad is being held up by sclerotic administration. That is working capital which small-time exporters cannot easily replace.

Worse, a $2bn suspected fraud by a diamond dealer in February has resulted in regulators banning certain types of bank guarantees that exporters use to ensure they get paid promptly, exacerbating their funding problems. These snafus come as many firms are still recovering from the ill-advised “demonetisation” of November 2016, when most banknotes were taken out of circulation overnight. The move snagged local supply chains, giving foreign rivals opportunities to fulfil orders that would have gone to hobbled Indian firms and to gain market share in India itself.

Those woes come on top of perennial frailties. Crippling red tape means most Indian firms are small: the country lacks the mega-factories hosting thousands of workers making T-shirts or mobile phones that are common elsewhere in Asia. All but a few firms lack the heft to participate in global supply chains. A relatively strong rupee in recent years has not helped.

Unwilling to enact labour and land-acquisition reforms that might foster larger firms, the Indian government is instead shielding its industry from foreign competition. In recent months it has imposed tariffs on a dizzying array of goods, from mobile phones to kites. Though those will no doubt help stymie imports, it is just as likely that trade measures imposed by other governments will hobble India’s exports.

For it is India’s misfortune that Donald Trump’s America is its biggest source of trade surpluses. Mr Trump’s administration has multiplied the salvos against India, whether decrying supposed export subsidies, making it harder for Indian IT workers to get visas or accusing India of artificially weakening its currency. Unlike many American allies, India has not been exempted from imminent steel tariffs.

India would be seriously damaged by any further escalation in trade conflicts. It needs hard currency from exports not only to finance imports and economic growth, but also to repay external debts. These have swelled to around $500bn, or roughly a fifth of GDP, more than 40% of which is due in less than a year.

-

-

India runs perennial trade deficits. Unlike China's, India's US$ reserves are not built by trade surpluses. India is heavily dependent on foreign debt and direct and portfolio investments for its US$ reserves.

As long the West sees India as a useful counterweight to China, the western money will continue to flow into India.

Here are a couple of excerpts from The Hindu Businessline on this subject:

https://www.thehindubusinessline.com/opinion/the-flip-side-to-build...

"Ample reserves are a source of comfort, but there are costs in managing them as well as risks due to debt and hot money flows"

"In BoP parlance, capital flows include equity flows (mainly foreign direct investment and portfolio investment) and debt flows (essentially consist of external commercial borrowing or ECB, NRI deposits, trade credit and portfolio debt investment). As per the IIP, debt liabilities account for nearly 48 per cent and carry the risk of debt service (repayment and interest payment). Portfolio equity investments are known as “hot” money or speculative money and as on March 2021, these flows accounted for 23 per cent of total liabilities. Thus, the forex reserves build-up has the potential risks of growing debt liabilities and facing the vagaries of “hot” money"

-

-

Russia and India reportedly halt talks over using rupees for trade, with Moscow preferring to be paid in Chinese yuan

https://ca.sports.yahoo.com/news/russia-india-reportedly-halt-talks...

Russia and India have suspended negotiations over using rupees for trade, Reuters reported.

Moscow, with a high trade gap in its favor, believes accumulating rupee is "not desirable."

China prefers to be paid in Chinese yuan or other currencies.

Russia and India have suspended negotiations over using rupees for trade between the two countries, with Moscow reluctant to keep the Indian currency on hand, Reuters reported Thursday.

The halt in talks deals a blow to Indian importers of cheap Russian oil and coal who were looking forward to a permanent rupee payment mechanism that would help bring down costs for currency conversion.

Russia, with a high trade gap in its favor, believed it would have an annual rupee surplus of more than $40 billion if a mechanism were enacted. Moscow felt that accumulating rupee is "not desirable," the report said, citing an unnamed official with the Indian government.

India's finance ministry, the Reserve Bank of India and Russian authorities did not immediately respond to requests from Reuters for comment.

Russia wants to be paid in Chinese yuan or other currencies, a second Indian government official involved in the discussions told Reuters. Moscow has increasingly turned to the yuan to move away from the US dollar after Russia was hit with Western sanctions for invading Ukraine in February 2022.

India began exploring a rupee settlement mechanism with Russia soon after Moscow launched war against the former Soviet state. No reported deals have been conducted using rupees, Reuters reported.

A currency dispute between Russia and India left deliveries of Russian weapons to India on hold, Bloomberg reported last month. The stalemate froze more than $2 billion in payments from India.

One factor that contributes to some countries not needing to hold rupees is India's share of global exports of goods, which runs at about 2%, the Reuters report said.

-

-

Geopolitics is shrinking India’s risk premium | Reuters

https://www.reuters.com/breakingviews/geopolitics-is-shrinking-indi...

India is also benefiting from worsening relations between Washington and Beijing. Companies are looking to shift supply chains out of the People’s Republic, while money managers need a place to deploy long-term funds with fewer risks of financial sanctions.

In some cases, the pivot is stark: Apple suppliers Foxconn (2317.TW) and Pegatron (4938.TW), for example, are building factories in Karnataka and Tamil Nadu. JPMorgan analysts reckon India will make one in four iPhones within two years, even though manufacturing costs are higher than in China. Ontario Teachers’ Pension Plan, Canada’s third-largest retirement fund, closed part of its China equity investment team based in Hong Kong in April, seven months after opening an office in Mumbai.

---------

MUMBAI, May 9 (Reuters Breakingviews) - Indian tycoons and financiers are sitting back as global business comes to them for a change. Apple (AAPL.O) CEO Tim Cook, Microsoft (MSFT.O) boss Satya Nadella and Blackstone (BX.N) President Jon Gray have all visited India this year. They are lured by a country whose potential as an alternative investment destination to China increasingly outweighs the local challenges of doing business.

Visitors see many attractions. India’s $3 trillion economy is forecast to grow by 6.5% this fiscal year, continuing to outpace the rest of the world. Plentiful imports of cheap Russian oil are keeping inflation in check. Meanwhile, the workforce of the world’s most populous country offers low costs, high numbers of technology engineers, and hundreds of millions of people who speak English.

Executives and investors also see a business-friendly government that is likely to remain in power for the next half-decade. Opinion polls suggest Prime Minister Narendra Modi will win a third term next year: the biannual Mood of the Nation survey, published in January, found 72% of respondents rated Modi’s performance as good, up from 66% in August. If he wins re-election with an outright majority, businesses would not have to worry about unpredictable coalition politics.

Yet India is also benefiting from worsening relations between Washington and Beijing. Companies are looking to shift supply chains out of the People’s Republic, while money managers need a place to deploy long-term funds with fewer risks of financial sanctions.

In some cases, the pivot is stark: Apple suppliers Foxconn (2317.TW) and Pegatron (4938.TW), for example, are building factories in Karnataka and Tamil Nadu. JPMorgan analysts reckon India will make one in four iPhones within two years, even though manufacturing costs are higher than in China. Ontario Teachers’ Pension Plan, Canada’s third-largest retirement fund, closed part of its China equity investment team based in Hong Kong in April, seven months after opening an office in Mumbai.

India appeals as more than a manufacturing base, though. Its economy also dangles the promise of Chinese-style growth. GDP per capita was $2,379 in 2022, less than one fifth of its eastern neighbour. Over 1.2 billion people have mobile phone connections; half of which are smartphones. Morgan Stanley analysts and strategists expect India to become the world’s third-largest economy and stock market before the end of the decade.

India remains a tricky destination for international companies and investors. New Delhi has a long-standing fondness for import tariffs and is infamous for wrangling over tax with multinationals including Vodafone (VOD.L) and energy group Cairn.

-

-

Geopolitics is shrinking India’s risk premium | Reuters

https://www.reuters.com/breakingviews/geopolitics-is-shrinking-indi...

India is also benefiting from worsening relations between Washington and Beijing. Companies are looking to shift supply chains out of the People’s Republic, while money managers need a place to deploy long-term funds with fewer risks of financial sanctions.

In some cases, the pivot is stark: Apple suppliers Foxconn (2317.TW) and Pegatron (4938.TW), for example, are building factories in Karnataka and Tamil Nadu. JPMorgan analysts reckon India will make one in four iPhones within two years, even though manufacturing costs are higher than in China. Ontario Teachers’ Pension Plan, Canada’s third-largest retirement fund, closed part of its China equity investment team based in Hong Kong in April, seven months after opening an office in Mumbai.

---------

MUMBAI, May 9 (Reuters Breakingviews) - Indian tycoons and financiers are sitting back as global business comes to them for a change. Apple (AAPL.O) CEO Tim Cook, Microsoft (MSFT.O) boss Satya Nadella and Blackstone (BX.N) President Jon Gray have all visited India this year. They are lured by a country whose potential as an alternative investment destination to China increasingly outweighs the local challenges of doing business.

Visitors see many attractions. India’s $3 trillion economy is forecast to grow by 6.5% this fiscal year, continuing to outpace the rest of the world. Plentiful imports of cheap Russian oil are keeping inflation in check. Meanwhile, the workforce of the world’s most populous country offers low costs, high numbers of technology engineers, and hundreds of millions of people who speak English.

Executives and investors also see a business-friendly government that is likely to remain in power for the next half-decade. Opinion polls suggest Prime Minister Narendra Modi will win a third term next year: the biannual Mood of the Nation survey, published in January, found 72% of respondents rated Modi’s performance as good, up from 66% in August. If he wins re-election with an outright majority, businesses would not have to worry about unpredictable coalition politics.

Yet India is also benefiting from worsening relations between Washington and Beijing. Companies are looking to shift supply chains out of the People’s Republic, while money managers need a place to deploy long-term funds with fewer risks of financial sanctions.

In some cases, the pivot is stark: Apple suppliers Foxconn (2317.TW) and Pegatron (4938.TW), for example, are building factories in Karnataka and Tamil Nadu. JPMorgan analysts reckon India will make one in four iPhones within two years, even though manufacturing costs are higher than in China. Ontario Teachers’ Pension Plan, Canada’s third-largest retirement fund, closed part of its China equity investment team based in Hong Kong in April, seven months after opening an office in Mumbai.

India appeals as more than a manufacturing base, though. Its economy also dangles the promise of Chinese-style growth. GDP per capita was $2,379 in 2022, less than one fifth of its eastern neighbour. Over 1.2 billion people have mobile phone connections; half of which are smartphones. Morgan Stanley analysts and strategists expect India to become the world’s third-largest economy and stock market before the end of the decade.

India remains a tricky destination for international companies and investors. New Delhi has a long-standing fondness for import tariffs and is infamous for wrangling over tax with multinationals including Vodafone (VOD.L) and energy group Cairn.

Twitter Feed

Live Traffic Feed

Sponsored Links

South Asia Investor Review

Investor Information Blog

Haq's Musings

Riaz Haq's Current Affairs Blog

Please Bookmark This Page!

Blog Posts

International Schools: Pakistan Ranks Among Top 5 Countries in the World

Pakistan ranks among the top 5 nations in terms of international schools offering schooling based on International Baccalaureate (IB) and IGCSE (Cambridge) curricula. China leads with 1,000 international schools, followed by India (900), UAE (784), Pakistan (598) and Brazil (415). The medium of instruction in these schools is English. …

Posted by Riaz Haq on April 19, 2025 at 8:00am

Pakistan Minerals Investment Forum Draws Interest of Global Investors

Pakistan's mineral resources, estimated to be over $6 trillion, attracted global investor interest at the Pakistan Minerals Investors Forum 2025 (PMIF2025) held recently in Islamabad on April 8th and 9th. It was attended by major international companies and government officials from Australia, Canada, China, Saudi Arabia, Turkiye, the US and other nations. …

ContinuePosted by Riaz Haq on April 12, 2025 at 11:30am — 3 Comments

© 2025 Created by Riaz Haq.

Powered by

![]()

You need to be a member of PakAlumni Worldwide: The Global Social Network to add comments!

Join PakAlumni Worldwide: The Global Social Network