PakAlumni Worldwide: The Global Social Network

The Global Social Network

Pakistani Economy Suffers From Sharp Decline in FDI and Savings Rate

Major Issues:

In a wide-ranging presentation to the Pakistan Club at the University of Chicago Booth School of Business, Mr. Chandna, an alumnus of the university, listed the following major issues facing Pakistani economy:

1. Pressure on capital account

2. Declining FDI

3. Declining tax to GDP ratio

4. Over reliance on monetary policy

5. Excessive domestic borrowing

6. Extremely volatile internal and external geo-political environment

7. Energy shortages

8. Increase in poverty and unemployment rates

Heavy Borrowing:

To make up for the shortfall in investments and tax revenues, the Pakistani government is forced to borrow heavily from commercial banks and international financial institutions such as the World Bank, the Asian Development Bank and the IMF, in addition to recent floating of $2 billion worth of bonds on international debt market. These debts add to the debt-to-GDP ratio and put further pressure on the cost of debt service.

Many of the problems highlighted by Mr. Chandna did not exist during President Musharraf's rule when foreign and domestic investments climbed to new highs and debt-to-gdp rartio declined.

|

| Pakistan Domestic Savings Rate Source: World Bank |

Domestic savings rate was about 18% and foreign direct investment reached $5.2 billion, or 3.5% of Pakistan's GDP. These investments fueled economic growth from 2000-2008. In my view, the activist judges led by former chief justice Iftikhar Mohammad Chaudhry have contributed significantly to the sharp decline in FDI and domestic investments in the country.

|

| Gross Fixed Capital Formation in Pakistan. Source: ADB |

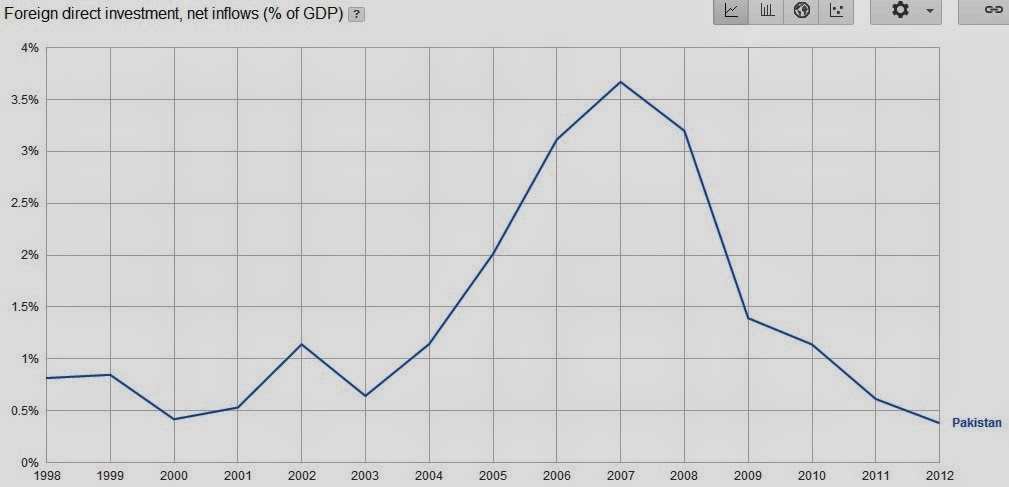

Foreign Direct Investment (FDI):

World Bank's data shows that foreign direct investment (FDI) in Pakistan reached a peak of over $5 billion (3.6% of GDP) in 2007 and then fell sharply in the wake of Justice Chaudhry's reversal of the privatization of Pakistan Steel Mills. FDI has essentially dried up and the Pakistan Steel Mills Corporation has accumulated losses over Rs. 100 billion in spite of multiple bailouts at taxpayers expense. It is currently operating at just 3% of capacity and its monthly payroll adds up to Rs. 500 million, according to Dawn.

|

| FDI as % of GDP in Pakistan Source: World Bank |

Canceled Privatization Deals:

Huge subsidies are being given at taxpayers' expense to Pakistan Steel Mills and several other state-owned enterprises which take resources away from more pressing needs for spending on education, health care and infrastructure. In fact, Pakistan Education Task Force Report 2011 reported that "under 1.5% of GDP [is] going to public schools that are on the front line of Pakistan's education emergency, or less than the subsidy for PIA, Pakistan Steel, and Pepco."

Speaking at a recent international judicial conference in Islamabad, Dr. Ishrat Hussain, current dean of the Institute of Business Administration and former governor of The State Bank of Pakistan, said there has not been a single privatization deal in Pakistan since the Supreme Court's 2006 decision voiding the steel mill transaction.

Dr Hussain said that despite fulfilling the legal requirements, the fear that the country’s courts may take suo motu notice of the transaction, and subsequently issue a stay order, deters businesses from investing in Pakistan, according to a report in The Express Tribune. “A large number of frivolous petitions are filed every year that have dire economic consequences. While the cost of such filings is insignificant the economy suffers enormously,” he added.

Crucial Projects Delayed:

Among other projects, Dr. Hussain particularly cited Reko Diq and LNG projects which could not proceed because of judicial activism of Pakistan Supreme Court judges.

The lack of progress on liquefied natural gas (LNG) deal has exacerbated Pakistan's energy crisis. It would have brought in 400 million cubic feet of gas per day to bridge the growing supply-demand gap now crippling Pakistan's economy.

The invalidation of Reko Diq license to Tethyan, joint venture of Canada's Barrick and Chile's Antofagasta, has turned away Pakistan's single largest foreign investment deal to date. The deposit in Balochistan was expected to produce about 200,000 tons of copper and 250,000 ounces of gold annually. Under the deal Baluchistan province would hold a 25 percent stake in the project, with Tethyan holding the remaining 75 percent.

Militants Released:

In addition to activist judges intervention in economic matters, there have also been many instance in which hundreds of known militants have been released by Pakistani courts. Those released have then committed acts of terror which have also scared away investors, both foreign and local.

Summary:

Mohsin Mushtaq Chandna's presentation of the data and facts is quite comprehensive. A combination of poor governance and activist judges have significantly contributed to the major issues highlighted in the presentation. I hope Prime Minister Nawaz Sharif's government is up to the tough challenges faced by Pakistan. Failure to confront these challenges would produced yet another lost decade like the decade of 1990s when Pakistan's economic growth was just 3-4%.

You can find a pdf version of Mr. Chandna's presentation on PakAlumni.com website:

http://www.pakalumni.com/forum/topics/assessment-of-the-state-of-pa...

Views: 444

-

Comment by Riaz Haq on June 16, 2014 at 9:02am

-

Here's an excerpt of Bloomberg story about Pakistani Taliban warning foreign investors and MNCs to leave Pakistan:

Pakistan’s military began a full-scale operation in the Taliban stronghold of North Waziristan, prompting insurgents to warn foreign investors, airlines and multinational companies to leave the country.

“We’re in a state of war,” Shahidullah Shahid, a spokesman for the Tehrik-e-Taliban Pakistan, or TTP, said in a statement today. “Foreign investors, airlines, and multinational companies should cut off business with Pakistan immediately and leave the country or else they will be responsible for their damage themselves.”

Related:

Pakistan Army Starts Offensive Against Taliban in Tribal Area

Pakistan Military Says 80 Terrorists Killed in N. Waziristan

The army said yesterday it would target local and foreign terrorists in North Waziristan, a tribal region near the Afghan border the U.S. has called the “epicenter” of terrorism. The operation, long sought by the U.S., comes a week after militants attacked the country’s biggest international airport.

As Islamic militants capture cities in Iraq and the U.S. draws up plans to withdraw from Afghanistan, public opinion in Pakistan is shifting in favor of stronger action against fighters who were previously seen locally as more of a threat to America’s interests. The Taliban wants to impose its version of Islamic Shariah law in Pakistan, which includes a ban on music and stricter rules for women.

Pakistan’s Future

“At stake is the future of Pakistan,” Mahmud Ali Durrani, a former national security chief and ex-ambassador to the U.S., said by phone. “Do we want a Talibanized Pakistan or do we want to live according to the constitution, democracy? If we want to live according to our constitution and democracy then we have to fight for it, because they are the kind of people who don’t believe in these things.”

Prime Minister Nawaz Sharif’s party won an election last year after pledging peace talks with the TTP, the group at the forefront of an insurgency that has killed 50,000 people since 2001. Negotiations that began in March collapsed over the TTP’s demands for prisoner releases even before progressing on issues such as Shariah law.http://mobile.bloomberg.com/news/2014-06-15/pakistan-army-strikes-a...

-

-

Here's a Dawn Op Ed by Dr. Ishrat Husain on Pakistan's isolation from global economy:

It is becoming increasingly difficult for Pakistanis to obtain visas to visit other countries of the world. Security clearances have made it difficult for businessmen to travel and explore opportunities. The resurgence of polio has further added to the existing problems. Even Sri Lanka has removed Pakistan from the list of ‘on arrival visa’ countries.

It is pertinent to probe the reasons that have led to our isolation.

The international Financial Action Task Force has placed Pakistan among a handful of countries in the high-risk category for its lack of action against money laundering and terrorism financing. Capital inflows and outflows from Pakistan are now subjected to more serious scrutiny. Even legitimate philanthropic donations for noble causes have to bear the brunt.International retail banks are either completely withdrawing or substantially curtailing their operations particularly at the retail level. Pakistani banks are facing difficulties in maintaining international correspondent banking ties. Pakistan is being edged out of international financial integration.

The country’s market share in world exports has declined significantly. The recent energy crisis can be blamed for short-term production difficulties but the withdrawal of the buying houses’ physical presence from the country has contributed significantly to this decline. New and emerging companies avoid Pakistan as they can source their supplies at competitive prices and quality from Bangladesh, Cambodia, Vietnam etc. where they can easily undertake reconnaissance and exploratory trips.

Karachi used to be once an international hub for air travel. Almost all reputed airlines used to route their operations through Karachi. Western airlines suspended their services in the 2000s and after the recent attack on the Karachi and Peshawar airports some airlines have cancelled flights or discontinued their services altogether. Pakistanis are now left with fewer choices for travelling abroad.

Insurance premia on shipping cargo and passengers escalated soon after September 2001 but slowly came down. In recent years, premia are becoming heftier, reinsurance getting difficult to obtain and several Western companies are unwilling to issue insurance policies to foreigners intending to visit Pakistan. The landed cost of goods at Pakistani ports is likely to rise due to this escalation in insurance premia. Alternatively, big shipping companies will simply skip our ports.

The northern areas of Pakistan that can be compared to the mountainous regions of Switzerland used to attract thousands of tourists from abroad every year for hiking, trekking, mountain climbing, skiing and other sports. The local economy of this area depends on the tourist trade. Since the murderous attacks on the tourists at the Nanga Parbat base camp tourist traffic has almost disappeared.

In the knowledge-based economy that is going to characterise the 21st century, Pakistani students, researchers and faculty suffer from a serious handicap as they do not get to meet any of their international counterparts at home and have great difficulty in getting opportunities to visit abroad. Collaborative research and exchange in natural and social sciences in which Pakistan used to feature prominently is waning rapidly.

Pakistani professionals used to dominate international organisations in both the public and private sectors. They had disproportionately high representation in senior decision-making positions. It is now difficult to find Pakistanis in top positions in any noteworthy public international organisation, or private multinational company. Pakistanis in higher positions were conduits for promoting business with the country of their origin as they understood the situation much better.

---------

http://www.dawn.com/news/1117090/delinking-from-global-economy

-

-

Sakib Sherani's Op Ed in Dawn on Pakistan's debt situation:

In overall terms, since July 2013, non-debt creating foreign exchange inflows (such as foreign direct investment, remittances and exports) have increased by $2.2bn, while debt flows have increased by $4.1bn (in net terms).

While Pakistan’s overall external debt situation is not alarming at the moment, with the bulk of the debt stock long-term and concessional in nature, and with debt repayment indicators in a relatively comfortable zone, the trend established in the past few years does give cause for concern.

The concern is accentuated by the possible confluence of a number of unfavourable factors in the medium term. Within the next three years, repayments begin on maturing sovereign dollar-denominated bonds; to the Paris Club on rescheduled debt; and to the IMF for the amounts disbursed under the current programme. In addition, imports relating to new power plants and the projects under the China-Pakistan Economic Corridor will also kick in. On top of all this, Pakistan could be incurring as yet unspecified external liabilities on CPEC projects.

With exports misfiring, the government paying inadequate attention to this cause, and remittances plateauing, the unfolding scenario could be the ‘worst case’ rather than the hopeful ‘base case’ constructed by the government and IMF.

(A crude indicator of the PML-N government’s priorities is the number of hours the finance minister has spent travelling the world meeting foreign bond investors in the past two years versus the amount of time he has given to Pakistan’s exporters in listening to, and trying to address their concerns.)

Taking external as well as domestic debt together, Pakistan’s debt dynamic in overall terms is extremely unfavourable. Public debt has increased nearly three-fold since 2008, rising to almost Rs18 trillion by end-June 2015, growing at a compounded annual rate of over 16pc. In the last two years, Rs3.2tr has been added to the public debt, increasing the stock by 22pc. Making the debt dynamic non-benign is the fact that the bulk of the increase (Rs2.7tr) has come from high-cost, shorter-maturity domestic debt.

With economic growth stagnating, inflation-adjusted increase in government revenues only nominally positive, and uncertain prospects for exports, the outlook for public debt is not benign. Already, public debt-to-GDP ratio stands at over 65pc (excluding the quasi-fiscal deficit), well above its legal threshold under the Fiscal Responsibility and Debt Limitation (FRDL) Act of 60pc. Interest payments are inching up, budgeted to consume 52pc of total net federal revenue (after provincial transfers) in the current fiscal year.

An oft-overlooked aspect of Pakistan’s debt situation is the political economy. There is an inherent asymmetry between the ‘benefits’ derived from new debt undertaken, and the burden of its repayment. There are two facets worth considering. First, those segments who tend to ‘benefit’ from the debt contracted (the elite) are usually different from those who bear the incidence of the debt burden (the less affluent).

The elite benefit from the country’s overall borrowing because it insulates them from difficult choices by easing their budget constraint. The debt expands their available resource pool, and their control and influence of expenditure allocation allows them to increase the spending on their constituencies while shifting the ‘burden’ and consequences to less influential segments. The consequences can be in the form of expenditure cutbacks, lower spending on public services, lower investment and growth in the economy and/or higher inflation.

-

-

Developing countries to dominate global saving and investment, but the poor will not necessarily share the benefits, says report

http://www.worldbank.org/en/news/feature/2013/05/15/developing-coun...

In less than a generation, global saving and investment will be dominated by the developing world, says the just-released Global Development Horizons (GDH) report.

By 2030, half the global stock of capital, totaling $158 trillion (in 2010 dollars), will reside in the developing world, compared to less than one-third today, with countries in East Asia and Latin America accounting for the largest shares of this stock, says the report, which explores patterns of investment, saving and capital flows as they are likely to evolve over the next two decades.

Titled ‘Capital for the Future: Saving and Investment in an Interdependent World’, GDH projects developing countries’ share in global investment to triple by 2030 to three-fifths, from one-fifth in 2000.

Productivity catch-up, increasing integration into global markets, sound macroeconomic policies, and improved education and health are helping speed growth and create massive investment opportunities, which, in turn, are spurring a shift in global economic weight to developing countries.

A further boost is being provided by the youth bulge. By 2020, less than 7 years from now, growth in world’s working-age population will be exclusively determined by developing countries. With developing countries on course to add more than 1.4 billion people to their combined population between now and 2030, the full benefit of the demographic dividend has yet to be reaped, particularly in the relatively younger regions of Sub-Saharan Africa and South Asia.

GDH paints two scenarios, based on the speed of convergence between the developed and developing worlds in per capita income levels, and the pace of structural transformations (such as financial development and improvements in institutional quality) in the two groups. Scenario one entails a gradual convergence between the developed and developing world while a much more rapid one is envisioned in the second.

In both scenarios, developing countries’ employment in services will account for more than 60 percent of their total employment by 2030 and they will account for more than 50 percent of global trade. This shift will occur alongside demographic changes that will increase demand for infrastructural services. Indeed, the report estimates the developing world’s infrastructure financing needs at $14.6 trillion between now and 2030.

The report also points to aging populations in East Asia, Eastern Europe and Central Asia, which will see the largest reductions in private saving rates. Demographic change will test the sustainability of public finances and complex policy challenges will arise from efforts to reduce the burden of health care and pensions without imposing severe hardships on the old. In contrast, Sub-Saharan Africa, with its relatively young and rapidly growing population as well as robust economic growth, will be the only region not experiencing a decline in its saving rate.

-

-

Pakistan received around $2 billion in foreign remittances, partly because of the seasonal effect of Eidul Azha.

The SBP is expected to officially announce the foreign remittances statistics next week.

https://tribune.com.pk/story/1501689/money-matters-pakistan-gets-23...

---------------

Pakistan has received two short-term loans worth $230 million from international creditors, meant to keep the official foreign exchange reserves at a level sufficient to provide cover to three-month import bill.

According to officials, the country received an amount of $153 million from Citibank in August. Besides, Islamic Development Bank (IDB) gave a $77 million short-term loan in July for crude oil import.

The IDB’s short-term facility is meant for import of crude oil from Saudi Arabia and the lender directly makes payments to the oil supplier on behalf of an oil importer. It partially helped lower pressure on the country’s forex reserves.

From April to May this year, Pakistan had signed three separate short-term loan agreements with the IDB valuing $700 million. Of this amount, Pakistan has already imported crude oil equivalent to $340 million.

For the current fiscal year, the government has estimated receiving $1.55 billion short-term loan from the IDB against the oil import facility.

--------

During the week ending August 31, 2017, the SBP’s reserves increased by $338 million to $14.681 billion due to official inflows, the central bank had reported on Thursday.

For almost one month, Pakistan was touching the three-month import cover border line as its reserves remained at around $14.3 billion.

In order to avoid downgrading in its credit ratings and keep the tap of budget financing open from the World Bank, Pakistan has to maintain its official foreign currency reserves above the three-month import cover level.

The finance ministry is currently making arrangements for floating about $1 billion worth of Sukuk Bonds by middle of November and a better credit rating will help lower the cost of borrowing. It had also raised $1 billion last year at 5.5% interest rate – the lowest rate on the Islamic bond that it ever paid.

The government was reviewing different options to keep the reserves above the level of three-month import bill. The options included incentives for expatriates to invest in Pakistani dollar-denominated bonds, more restrictions on imports and steps that will encourage exporters to bring back export proceeds.

Finance Minister Ishaq Dar on Friday held a meeting with his Chinese counterpart Xiao Jie and discussed issues of mutual interests – including ways and means to further enhance bilateral economic relations.

During FY2016-17, Pakistan had borrowed a record $10.1 billion external loans that included a record-breaking $4.4 billion short-term financing.

Out of this, $2.3 billion came from Chinese financial institutions. The government took $1.7 billion from the China Development Bank, $300 million from the Industrial and Commercial Bank of China, and $300 million from the Bank of China.

It also obtained $445 million from the Noor Bank of the UAE, $650 million from a consortium of the Suisse Bank, the UBL and the ABL, $275 million from Citi and $700 million from the Standard Chartered Bank, London.

This was the first time in Pakistan’s history that any government has taken over $10 billion as fresh foreign loans in a single year.

Pakistan Tahreek-e-Insaf Chairman Imran Khan on Thursday called Finance Minister Ishaq Dar Pakistan’s economic hitman while criticising his economic policies.

In July, Pakistan obtained a total of $254.9 million loans, including $77 million from IDB. It received $75 million from the World Bank for project financing.

China also gave $71.5 million worth of loans for carrying out various Beijing-funded schemes. The Asian Development Bank provided $28.8 million worth of loans.

The $254.9 million loans were 3.2% of the total annual budgetary estimates of $8 billion for FY2017-18.

-

-

THE EXPRESS TRIBUNE > OPINION

Economy: real and monetary

By Dr Pervez TahirPublished: March 16, 2018

https://tribune.com.pk/story/1661121/6-economy-real-monetary/

A debate is raging that the economy is in dire straits and the continuation of present policies is a recipe for complete disaster. Any economy has two sides, the real and the monetary-financial. The disaster story relates to the latter. The classical economists used to think that money is merely a veil and what matters is the real economy of goods and services.

It was, however, Lord Keynes who discovered that the Great Depression of the 1930s was caused by insufficient demand for the existing industrial capacity. Boosting demand by printing currency would revive the economy. He was concerned with the short run in which money does matter. Classical economists were talking of the long run over which the industrial capacity is created. Long-term growth is what matters in developing economies like Pakistan. Investment is the strategic variable along with a proper choice of technique to employ the growing labour force. The chosen technique can be labour-saving, labour-intensive, or labour-absorbing. The last-mentioned was prescribed by the celebrated Cambridge economist Joan Robinson in the case of China. (Incidentally, besides being a woman, her love for China cost her the Nobel prize.)

In Pakistan, the cohabitation of political transitions and economic crisis is a familiar sight. The story line begins with the external sector and the government sector in terms of financial and monetary indicators. For the February 2008 elections, the transition fiscal year was 2007-08. Total debt was 63.2% of GDP and the external debt and liabilities were 30.7% of GDP. The SBP’s liquid reserves were 8.8 billion dollars, covering imports of 17 weeks. Short-term external debt was 8.2% of reserves. Inflation, current account deficit and fiscal deficit at 12%, 8.5% and 7.6% had all crossed danger zones. GDP growth of around five per cent was the lowest in five years. The economy was clearly on the downhill, touching the bottom at 0.36 in 2008-09. The transition fiscal year for elections in May 2013 was 2012-13. Total debt was 69.5% of GDP and the external debt and liabilities were 26.3% of GDP. The SBP’s liquid reserves were 6.1 billion dollars, covering 14.3 weeks’ imports. Short-term external debt was 4.4 % of reserves. The rate of inflation, current account deficit and the fiscal deficit were 7.4%, 1.1 % and 8.2%, respectively. GDP growth was low at 3.7%, but the economy was on the upturn. For the 2018 elections, 2017-18 is the transition fiscal year. The source of information for the year is the latest press release of the IMF, an organisation concerned mainly with the monetary and financial side of the economy. It expects fiscal deficit at 5.5 per cent, current account deficit at 4.8 per cent and GDP growth at 5.8 per cent. As a result, ‘risks to Pakistan’s medium-term capacity to repay the fund have increased’. Remember Ishaq Dar’s refrain that he had to go to the IMF to repay the debt contracted by the previous government. Free of political compulsions, the caretaker government had prepared the ground for it. The deal was to pay back without reform. The signs of slowly increasing growth were ignored.

Are we heading for a repeat of the script? The deputy head of the IMF has already made it clear that the possible grey-listing by the FATF does not disqualify a member to access its lending. The upturn in the real economy continues. CPEC investment will boost it further. The country has the ability to grow out of the present financial strife. Reform must be undertaken, but without repeating the mistake of the anti-growth IMF support.

-

-

Why #India’s '#Modi-fied' #GDP Math Lacks Credibility: How can #India's gdp growth rate be faster under #Modi government when its investment-to-gdp is down from 38% under UPA #Manmohansingh government to 30.3% now? How's capital-to-output ratio way up? https://thewire.in/political-economy/why-indias-new-gdp-math-lacks-...

India’s back-series GDP (gross domestic product) data, released by the NITI Aayog just four months before the 2019 general elections, turns the basic laws of macroeconomics on their head.

Here’s one that is most intriguing. The data shows lower GDP growth during the UPA years, which is when the gross investment to GDP ratio was peaking at 38%. And conversely, it shows higher GDP figures during the four years of Modi-led NDA-II government, which is when the gross investment to GDP ratio was at its lowest, at 30.3%.

Economic theory has always held that higher investments lead to higher GDP. So how can GDP grow faster when the investment-to-GDP ratio has fallen?

Technically, the only circumstance in which this can happen is when the economy’s productivity or the ‘Incremental Capital Output Ratio’ (ICOR) improves equally dramatically. Simply put, it means the economy generates a lot more output for the same amount of capital employed. There is no sign of that happening during the Modi government’s four years in which productivity was in fact negatively impacted by the twin shocks of demonetisation and messy GST implementation. Besides this, much of the NDA-II period has also seen the largest quantum ever of unproductive assets locked up in the form of non-performing assets (NPAs). Banks are not lending because of unresolved bad loans. How can productivity surge in such circumstances?

Says Mahesh Vyas, CEO of the Centre for Monitoring Indian Economy, a reputed private data research firm, “The new GDP back series numbers show India to be a magical economy where when the investment ratio drops sharply, the economy accelerates sharply. During the period (2007-08 to 2010-11) when the investment to GDP ratio was peaking at average 37.4% the average GDP growth was 6.7%. And in the recent four years (2014-15 to 2017-18) when the investment ratio was down to 30.3% the economy was sailing at 7.2%. Is this productivity magic?” There is really no answer to this fundamental questIon.

Former head of the Central Statistics Office (CSO) and chairman of the National Statistical Commission, Pronab Sen, is known to have a great feel for data and has been one of India’s foremost economists and chief statisticians. Sen has been critical of the manner in which the back-series data was essentially released by NITI Aayog and not by the CSO alone, as has been the practice in the past. This is tantamount to politicising institutions which deal with national statistics.

That apart, Sen also agrees that the back-series data does not pass the basic smell test linked to ground realities. While better productivity can theoretically produce higher output with the same quantum of capital or labour, he argues that the period of 2005-2012 also saw a big communication revolution in India due to mobile penetration. Consequently, it would be difficult to argue lower productivity in the UPA era. The service sector overall – whether communications, banking, real estate or hotels – clearly boomed during the UPA period.

Significantly, average GDP growth has been lowered to 6.7% during the UPA period in the new series, from over 8% in the earlier series, largely based on adjusting the service sector output (which was the biggest contributor to GDP) to lower levels.

There are other basic common sense tests which the new series fails. For instance, UPA-era growth is supposed to be lower even though the country’s exports were booming at 20%-plus, bank credit to industry grew at over 20% and the corporate earnings of the top 1,100 companies grew at at over 20%.

Comment

Twitter Feed

Live Traffic Feed

Sponsored Links

South Asia Investor Review

Investor Information Blog

Haq's Musings

Riaz Haq's Current Affairs Blog

Please Bookmark This Page!

Blog Posts

World Bank: Pakistan is 88% Urbanized

The World Bank researchers have recently concluded that 88 per cent live in urban areas. Their conclusion is based on satellite imagery and the Degree of Urbanization (DoU) methodology. The official Pakistani figures released by the Pakistan Bureau of Statistics (PBS) put the current level of urbanization at 39%. The source of this massive discrepancy is the government's reliance on administrative boundaries rather than population density and settlement patterns, according to the World Bank…

ContinuePosted by Riaz Haq on December 7, 2025 at 5:30pm

IMF Questions Modi's GDP Data: Is India's Economy Half the Size of the Official Claim?

The Indian government reported faster-than-expected GDP growth of 8.2% for the September quarter. It came as a surprise to many economists who were expecting a slowdown based on the recent high-frequency indicators such as consumer goods sales and durable goods production, as well as two-wheeler sales. At the same time, The International Monetary Fund expressed doubts about the Indian government's GDP data. …

ContinuePosted by Riaz Haq on November 30, 2025 at 11:30am — 2 Comments

© 2025 Created by Riaz Haq.

Powered by

![]()

You need to be a member of PakAlumni Worldwide: The Global Social Network to add comments!

Join PakAlumni Worldwide: The Global Social Network